How much Life Insurance do I need?

I often get asked by people “how much Life insurance do I need?” The majority of people haven’t a clue how much life insurance they need so don’t worry if you are unsure yourself. This article aims to point you in the right direction for the amount of life insurance that you actually need based on your personal circumstances. In general Life insurance is designed to protect your family financially until your children are financially independent. I know it’s a pretty grim subject but keep reading! The idea is to replace your earnings if something was to happen to you. This will keep your family’s lifestyle the same if you die. A mistake people can make is they want the same cover as their friend, but is the friends plan suitable?

So how do I calculate the amount I need?

So consider what your net wages are (life insurance benefits are tax free if you are married). For example, a married couple on €3000 net each and two kids the youngest baby John aged 1. Our couple live in Dublin and pay a mortgage of €1000 per month with 30 years to go on their loan. Based on this income level If you died tomorrow your family would lose €864,000 of earnings up until your youngest child is aged 25.

Now that’s not to say that after your death, your wife or husband goes on to remarry a handsome/beautiful richer husband or bride and the kids fall in love with them and live happily ever after.

But if we assume that does not happen life insurance is a good alternative:)

So do I really need €864,000 worth of cover? She might kill me in my sleep I hear you say!

Let’s think about it for a minute. If you died tomorrow what would come into the household and what bills would go away? So if you are married the good news is that the government will pay you a widow’s pension of €208.5 per week. So this equates to €260,208 in our example up till baby John is 25. Next you can consider that your mortgage would be cleared assuming you have mortgage protection so that frees up an additional €1000 per month that the family had been spending while you were alive.

Based on the example above the amount of cover to replace your income would be €315,792(Table 1). If you had a pension worth €100,000 then you only need €215,792.

Table 1: Life Insurance needs Calculation:

| Age of youngest | 1 |

| Income | 36000 |

| Amount required | 864000 |

| less widows pension | 260208 |

| less life insurance/pension | 0 |

| Mortgage repayments | 1000 |

| less mortgage repayments | 288000 |

| Total lump sum required | 315792 |

Once you have calculated how much you need there are several ways of getting the plan that’s suits you the most.

Types of Life Insurance plans:

There are loads of different types of life insurance plans on the market including

- level term

- Decreasing term and

- monthly income on death to name a few.

So if we take our example above consider the following:

“I only need €315,792 at this point in time in my life. Next year when baby John is 2 I won’t need as much cover as there will only be 23 years until he becomes 25 and the following year I need less again so how do I avoid overpaying for what I don’t need?”

Plans that fit the need perfectly:

In order to avoid paying more than you need to, the plans that fit the need the best are:

- Decreasing term (often marketed as mortgage protection) and

- monthly income on death

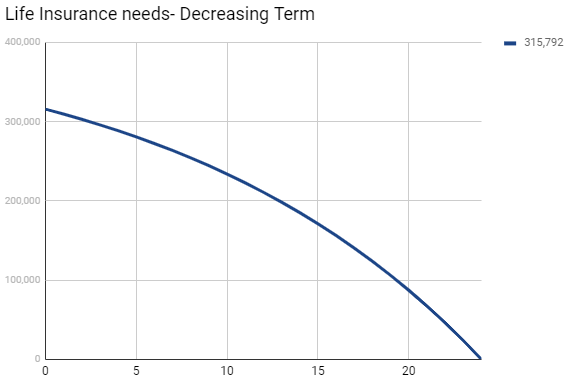

Decreasing term does what it says on the tin. It will decrease over time. In 24 years time when little John has become Big John the plan will have decreased down to zero. It is one of the most affordable ways(€21.49 for dual life plan based on both parents 35 next birthday and non smokers) to get the cover you need.

It looks like this over time :

Fig 1: Life Insurance needs

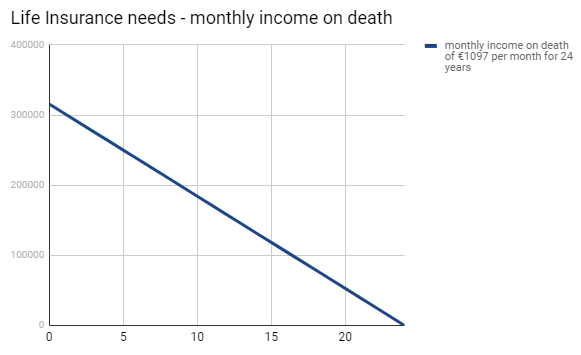

Similarly monthly income on death ( in this case it would equate to €1097 per month. Don’t forgot your mortgage of €1000 per month has disappeared and the government are paying you €208.5 per week) is a very affordable option (€20.11 for dual life plan based on both parents 35 next birthday and non smokers) to get the cover you actually need.

Fig 2 shows that if you died in the early years more would be paid out than if you died towards the end. It is similar to decreasing term except you receive the benefit in monthly instalments.

Fig 2: Life Insurance needs

If you would prefer extra cover above your needs:

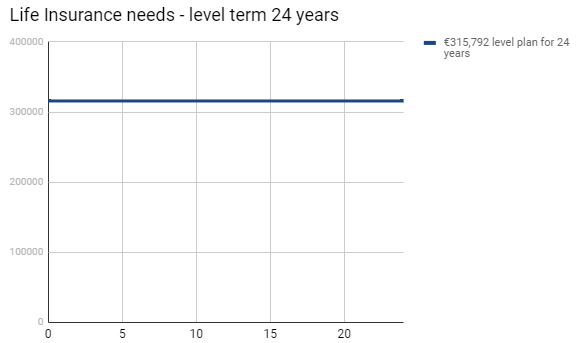

Many people prefer the level lump sum option for 24 years but it will cost more (€36.18 for dual life convertible plan based on both parents 35 next birthday and non-smokers). The benefit of this type of plan is that you could potentially extend the plan if you had convertible cover beyond 24 years.

Fig 3: Life Insurance needs

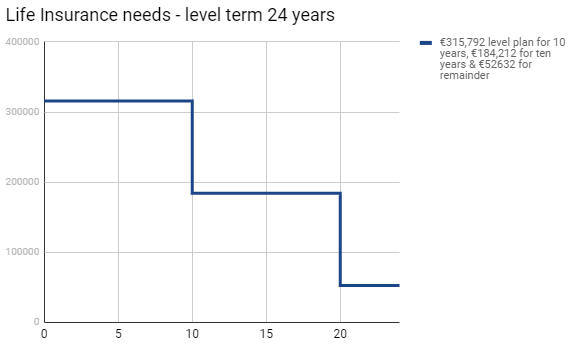

If you prefer having larger cover in the early years you could consider a ten year plan of €315,972 and then reevaluate your needs in ten years time.( €27.54 for dual life convertible plan based on both parents 35 next birthday and non smokers). As long as you have convertible cover you will be able to extend the plan no questions asked for a further ten years. However in ten years time your premium will go up as you will be ten years older. Fig 4 below shows this approach.

Fig 4: Life Insurance needs:

There are loads of add on benefits you can put into the above plans such as serious illness cover, personal accident cover and hospital cash, but if you are just looking for an affordable plan to cover you on death only then this article should help you. The plans above are designed to try and be a fit for your personal circumstances. It is worth talking to your financial advisor to talk about any other needs you may have. Have a read over what life insurance is best on the market as the plans above are suited for your basic essential needs. Best life insurance plan is another matter as there are some terrific plans that can pay your family more than you pay in. Check it out.

If you have any questions in relation to this article you can contact me at sean@financiallife.ie or call me on 015823524 and I would be happy to help.

You may also like:

Insurance

Insurance  Pensions

Pensions  Insurance

Insurance  Insurance

Insurance